Expect Big Change in Big Food

Expect Big Change in Big Food

A look at the sector's recent spin-offs and why more are likely

Why do large public companies pursue transformational business changes, like selling off assets or splitting into two separate companies? It’s not because they think it will be fun or that management is bored. It’s usually because their stock performance has lagged versus their peer group and major change is required to turn things around.

Shareholders want to be passive owners. They might actively manage their portfolios, and may occasionally talk to management, but they’re not managing these companies. Instead, they vote in boards — diverse groups of experienced and influential executives from across industries — to ensure they’re getting their required returns. To accomplish that, boards try to hire the right CEOs. CEOs then manage the business, and to do that well, they hire people who can do what they can’t.

The buck really stops with the board. Their most important job is to ensure those returns. So to judge their performance, the benchmarking analysis boards almost always start with is Total Shareholder Return (TSR) over, say, a 10 year period. TSR measures the return of an equity investment assuming that any dividends are immediately reinvested in the stock versus simply looking at the change in the stock price between two periods (i.e. price return).

When a company’s TSR begins to lag its peer group significantly, its board risks activist fund involvement as these specialist and slightly more “active” investors perceive an opportunity to effect (or force) change in order to boost those returns. And this typically includes a proposal to replace board members deemed more up to the task — i.e. partners at or friends of the activist fund. This risk is especially stark for companies that lack shareholder protections such as supermajorities held by families or foundations (more on that below).

But to avoid such a fate, boards can demonstrate the humility, skill, and will required to effect change proactively. Depending on what they (or their management consultants or investment bankers) determine to be the problem(s), a course of action can include things like replacing members of the c-suite, announcing a restructuring or cost-cutting plan, executing synergistic or strategic/growth M&A, or spinning-off assets or splitting the company.

The latter can be the most turbulent path if the spin-offs are large and transformational, but also the most effective in the event those business units or brands have become dis-synergistic over time, have developed radically diverging capital requirements, or — simply put — management lacks the resources, skill, or focus required to effectively manage and grow those businesses relative to others.

The distraction of non-core or dis-synergistic businesses can be so detrimental to long-term shareholder returns that risking the near-term distraction and strain associated with pulling a business apart at its seams becomes a value-accretive pursuit. Diverging business units can also depress a company’s earnings multiple as investors come to believe that each respective business lacks the attention and resources it deserves, thereby dragging down the value of the combined enterprise.

Over the last 10-15 years, there have been 4 large and notable spin-offs in CPG. 3 of these 4 are Big Food companies largely playing in snacks and “center store” grocery.

Kraft’s (since renamed Mondelez) spin-off of its “center of store” grocery unit (retained the Kraft name) in 2012.

Conagra’s spin-off of its Lamb Weston commercial potato and fry business in 2016.

GlaxoSmithKline’s spin-off and merger of its OTC consumer healthcare unit Pfizer’s consumer unit into a new JV in 2018, which then IPO’d as Haleon in July 2022.

Kellogg’s (renamed Kellanova) spin-off of its North American cereal unit (named WK Kellogg) in 2023.

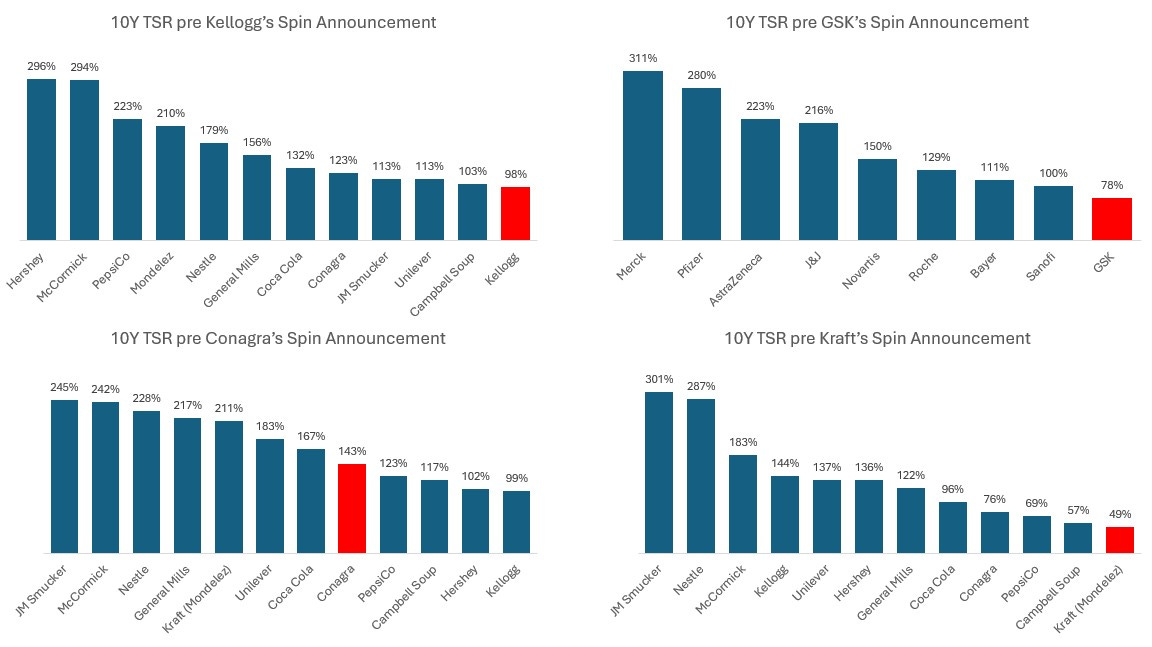

Let’s take a look at the TSRs for each of these companies versus their peer groups over the 10 year period prior to their spin-off announcement dates.

Notice anything?

All four of these companies were at or near the bottom of their peer sets on 10Y TSR.

Conagra’s position in particular was much closer to the bottom practically speaking than the chart depicts. While its 143% TSR (9.3% CAGR) was respectable albeit below average/median, the four companies to its right were either “untouchable” or already locked in their own battles with activist investors. PepsiCo had been battling Nelson Peltz’ Trian Partners beginning in late 2013, which publicly advocated for the separation of its beverage and snacks (Frito-Lay) businesses, including the potential merging of Frito-Lay and Mondelez. Campbell Soup has almost impenetrable shareholder protections in the form of a ~2/3rds super majority vote held by siblings Mary Alice Malone and Bennett Dorrance — two of the grandchildren of condensed soup inventor John T. Dorrance. Hershey is ~80% controlled by The Hershey Trust Company, a charitable trust that oversees the Milton Hershey School in Pennsylvania. And Kellogg is almost one-quarter owned by the W.K. Kellogg Foundation (~17%) and billionaire Gordon Gund (~6%) and, no doubt alarmed by its own underperformance, announced its multi-year “Project K” cost-cutting plan in 2013 and then of course announces the spin-off its cereal business in 2022.

This is all to say that Conagra didn’t have much cushion on its right flank.

Sure enough, JANA Partners began building a stake in Conagra in June 2015. They pushed the company to spin Lamb Weston as a non-core dis-synergist asset, and to outright sell its ill-fated and distracting Ralcorp private label business to TreeHouse Foods the year prior.

The timing of GlaxoSmithKline’s 10-year underperformance coincided with prior CEO Sir Andrew Witty’s retirement in 2017. Emma Walmsley, a long-time exec from L'Oréal, took over as CEO and shortly after announced the spin-off of its OTC consumer health business into a new JV/merger with Pfizer’s OTC unit. That business then IPO’d as a completely separate business called Haleon in 2022, but not before continued lackluster returns attracted interest from Elliott Investment Management in 2021.

As for Kraft, Peltz’s Trian, Bill Ackman’s Pershing Square, and Buffett’s Berkshire had all built single-digit stakes in the company. Peltz in particular had pushed Kraft’s CEO Irene Rosenfeld to acquire Cadbury in 2010 before then spinning off the grocery unit. Then only a few years later in 2015, Buffett partnered with 3G Capital and merged Kraft’s grocery business with Heinz, creating Kraft Heinz.

The goal of a spin-off is to improve shareholder returns. But this begs the question: which shareholders? Is it the long-term shareholders that plan to hold both stocks? Or new shareholders getting in after a spin-off when the respective stories are “cleaner” and they can chose whether to buy one, the other, or both in any combination?

For example, if you bought and held Conagra stock 10 years ago — meaning you held on to your Lamb Weston distribution and then continued reinvesting dividends from both Conagra and Lamb Weston — then your TSR today would be about 132% or an 8.8% CAGR — a tad below the pre-spin CAGR (Conagra’s TSR up to the spin date was 72%, since the spin Conagra’s TSR is negative 5% but Lamb Weston’s TSR is 170%). So, the spin-off was tremendous for investors that decided to dump Conagra stock and only own Lamb Weston, but a real disappointment for Conagra-only investors who were hopeful that shedding its food service and private label businesses would unlock more innovation and focus within the remaining branded packaged food units.

I do think it’s fair to give management and boards at least some credit for a spin-off increasing in value, but not forever. We can only judge their longer-term post-spin performance based on what they’ve continued to manage, not what they let go.

Meanwhile, if you had bought and held Kraft stock 15 years ago — meaning you held both Mondelez and Kraft Foods post-spin in 2012 and reinvested dividends, then held Kraft through the 2015 merger with Heinz while also reinvesting both regular dividends and the $16.50 special dividend paid to Kraft shareholders — then your TSR today would be about 343% or a 10.4% CAGR — much better than the 4% CAGR before the 2012 spin. However, your Kraft Heinz position would have been a major drag with its 36% negative TSR since the 2015 merger. If you had swapped your Kraft Heinz shares for Mondelez at the merger, your TSR would have been about 520%.

Seen another way, spin-offs offer shareholders more opportunities to make their own capital allocation decisions rather than boards or management toggling their time and attention inefficiently between large business units.

As far as GSK and Kellanova go, it’s only been a few years and so too early to judge.

JANA ended up exiting Conagra in 2022. 3G sold the last of its Kraft Heinz stake earlier this year, but Buffet remains a 26% owner. Yet in 2019 he admitted that Berkshire had overpaid for Kraft.

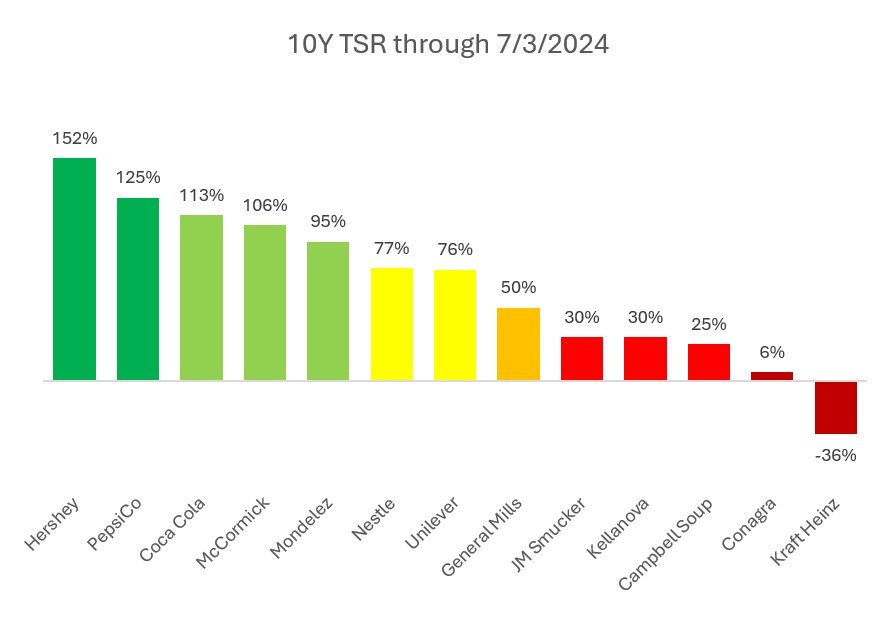

Packaged food is a tough business and center-of-the-store grocery is perhaps the toughest category in food for so many reasons — private label share gains and shifting consumer preferences towards whole foods, beverage, and snacking are two big ones.

I believe activists are likely to come back to Big Food unless even more radical changes come first at these companies. Maybe JANA and 3G have moved on, maybe Buffett is apathetic, maybe there is some food fatigue amongst leading activist funds, maybe all hope is lost for the grocery category — but changes must come.

JM Smucker, Kellanova, and Campbell all have significant family-related shareholder protections or super majorities, but they’re not oblivious to their underperformance (see below) and have been trying to transform their businesses on their own terms. But we haven’t yet seen the returns. General Mills is trying to make changes — selling its Yoplait business and buying more pet food companies. Unilever is selling its ice cream unit. Nestle’s gigantic $250B market cap makes it difficult for activists to build influence, but it too spun off its confection, water, and frozen pizza businesses among other changes. The rest of Big Food is performing better, but far below the rolling triple-digit 10Y TSRs investors were used to in the 2000s and early 2010s when consumer staples traded at premiums to the S&P500.

Expect more, likely even bigger changes soon.

Subsiding inflation should help mitigate the political blowback of any major shareholder-friendly corporate actions in Big CPG/Food. For example, should Conagra’s growthier snacks business (i.e. Slim Jim and Angie’s Boom Chicka Pop) really live alongside its Healthy Choice and Banquet frozen entrees businesses? How many more pet food businesses will General Mills acquire before that business should live independently? Should an activist revive old talks of merging Mondelez and Frito-Lay? Why should Campbell Soup manage a large snacks business alongside its flagship meals and sauces portfolio?

We can have endless fun speculating, but know that underperformance can only be tolerated for so long.

Disclosure: Author owns stock in General Mills, Conagra, Kraft Heinz, Hershey, PepsiCo, and Berkshire Hathaway.